Basic

CIT Appeals

CIT Appeals

ITAT Appeals

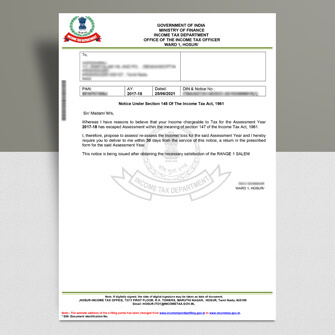

Regular IT Assessment

Reply of Notices 142(1), 147, 144, 143(2)

Other Related Services

GST Registration, Invoicing, GST Filing, TDS Return Filing, Accounting, Income Tax Return (ITR) Filing, Banking and Payroll

GST Invoice

Get GST eInvoice with Input Tax Credit